The Assumption Most People Make

Most HSA holders believe their provider is tracking spending in some meaningful way. That when they swipe the card at CVS, someone somewhere is recording that the $47 was for amoxicillin and not for shampoo.

Nobody is recording that. Not the HSA provider. Not CVS. Not the IRS. The only person who could record it is you.

This is not a failure of the system. It is the system working exactly as designed. Understanding why changes how you use your HSA.

What Your HSA Provider Actually Does

Your provider has three jobs:

- ●Hold your money in an account

- ●Process transactions when you swipe the card or request a transfer

- ●Report your total distributions to the IRS once a year

That third job is the one that matters here. At year-end, your provider sends a 1099-SA to the IRS. It contains one number: total distributions.

Not "total medical distributions." Not "total qualified distributions." Total distributions. One number. No categories. No line items. No receipts.

| What your provider reports to the IRS | What they do not report |

|---|---|

| Total distributions for the year | What each distribution was for |

| Total contributions for the year | Whether expenses were qualified |

| Account type (HSA) | Receipts or documentation |

That is the entire scope of their obligation. The IRS gets a single dollar figure. Everything else is on you.

Why They Do Not Track Your Spending

This is not laziness. It is structure.

Your HSA provider is a financial institution. Regulated as a bank or trust company. Their job is custody of assets and execution of transactions. Verifying whether your Walgreens purchase was bandages or breath mints is not in their charter.

Think about your checking account. Your bank processes debit card transactions at Target and Amazon. They never ask what you bought. They do not verify your purchases were reasonable. They move money. That is the job.

Your HSA provider operates the same way, plus the 1099-SA at year-end. But the 1099-SA is a financial report. Not a medical report.

Some providers offer receipt storage features. A few let you upload documents alongside transactions. But these are optional extras, not core functions. They are almost never promoted because they add cost and liability without generating revenue.

How Your Provider Makes Money

Your HSA provider makes money three ways.

Account fees. Monthly maintenance fees, per-transaction fees, paper statement fees. These apply whether your money moves or sits still.

Investment fees. If you invest your HSA balance, the provider earns from fund expense ratios, management fees, or custodial charges. Typically 0.30% to 0.50% of assets per year, according to Devenir's HSA survey data.

Cash sweep interest. Uninvested cash in your HSA earns interest. Your provider pays you a fraction of what that cash actually earns. The spread is revenue.

All three have something in common. The provider earns more when your money stays in the account. Invested money generates management fees year after year. Uninvested cash generates sweep revenue. Money that leaves the account generates nothing.

This does not mean your provider wants you to lose receipts. It means they have zero financial incentive to help you track spending or remind you to save documentation. Teaching you to save receipts does not generate revenue. Teaching you to invest more does.

A receipt tracking system would help you the most. It is the feature they are least motivated to build.

The Gap in the Middle

Here is the chain of responsibility for every HSA distribution:

You pay for a medical expense.

Your provider moves the money and reports the total to the IRS.

The IRS receives the total and trusts you to prove expenses were qualified.

The gap is obvious. Your provider passes a number to the IRS. The IRS expects you to substantiate it. Nobody in the middle does the matching. The layer that connects "I spent $47 at CVS" to "it was for a prescription antibiotic" does not exist unless you create it.

Your provider will never fill that gap. Not their job. No reason to make it their job. The IRS will not fill it either. They show up after the fact, asking for proof.

This is not a conspiracy. The HSA was designed as a tax-advantaged savings vehicle. The record-keeping requirement was assigned to the account holder. The tools to make that easy were left to the market.

The Debit Card Makes It Worse

Counterintuitive. The HSA debit card feels like the most responsible way to use your HSA. Swipe, done, tax-free.

But the debit card creates the biggest documentation problem. Money leaves immediately. No reimbursement process forces you to attach a receipt. No pause between "I spent this" and "I need to prove this."

Compare that to the delayed reimbursement approach. Pay out of pocket, reimburse later. The reimbursement itself is an event. You log in, request a distribution, match it to a receipt. The process has a built-in documentation step.

The debit card removes that step. Frictionless spending is great for user experience. Terrible for record-keeping.

Your provider loves the debit card. It keeps you engaged with the account. Makes the HSA feel useful and easy. But it creates a documentation blind spot that can cost thousands if the IRS asks questions.

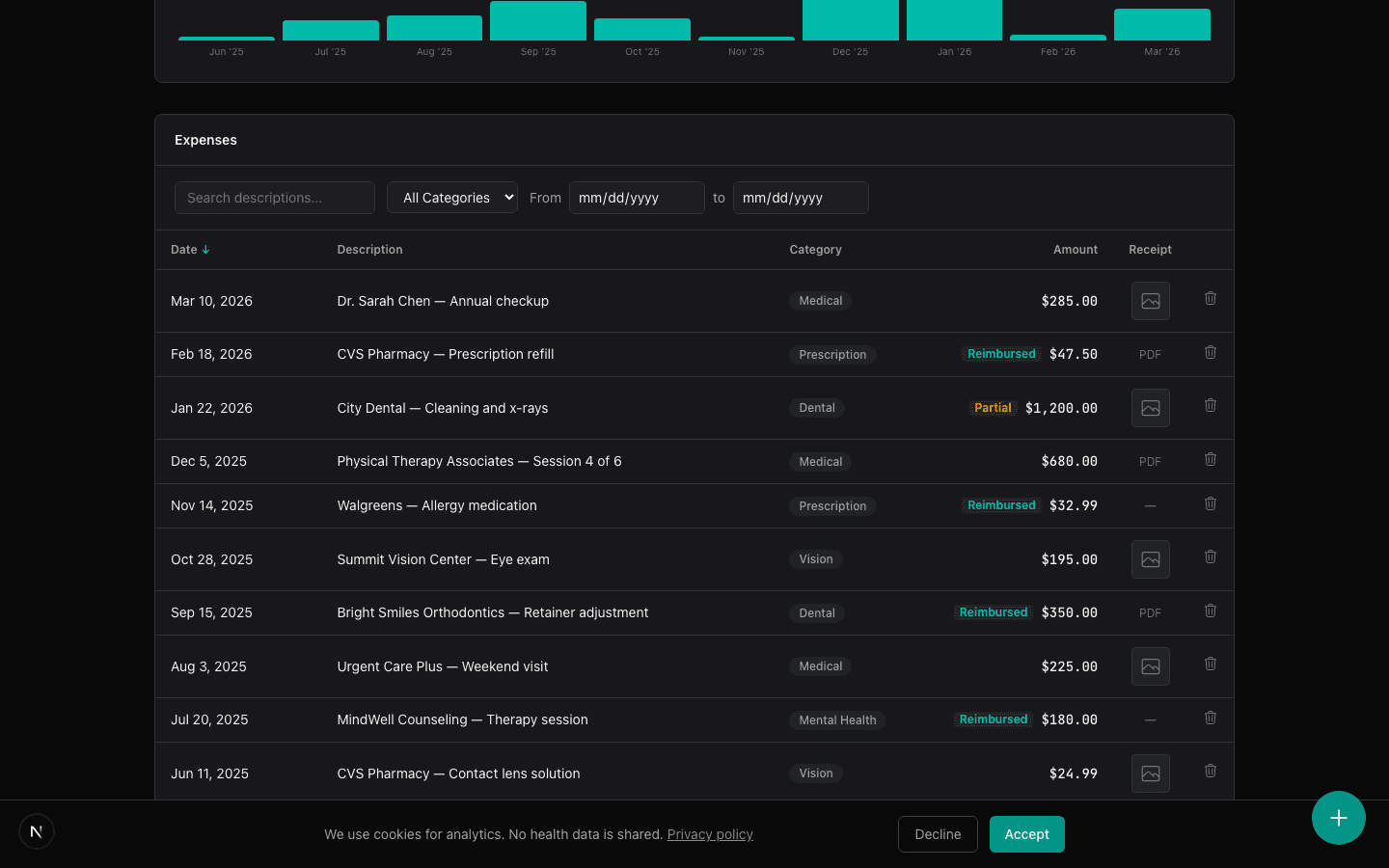

What a Real Paper Trail Looks Like

For every HSA distribution, qualified proof requires five elements:

- ●Date of the medical service or purchase

- ●Provider name (doctor, pharmacy, hospital)

- ●Amount you paid

- ●Description of the service or item

- ●Image of the receipt, bill, or EOB

Your card statement gives you #1, #2, and #3. It never gives you #4 or #5. Those two missing elements are the difference between "I paid CVS $47" and "I bought a prescribed antibiotic at CVS for $47."

The IRS cares about #4. Without it, your distribution is unsubstantiated.

The Long-Term Math

A 35-year-old saving $300/month in qualified receipts and using the delayed reimbursement strategy accumulates $72,000 in reimbursable expenses by age 55. The HSA stays invested that entire time. At 7% annual returns, the invested portion grows well beyond the original contributions.

Your provider earns 0.30% to 0.50% per year on every dollar that stays invested. You earn the growth. But only if you can prove the expenses later.

Every receipt is a future tax-free withdrawal. Every missing receipt is a withdrawal you can never take. At a 22% tax bracket plus the 20% penalty, $72,000 in unsubstantiated distributions costs you $30,240 in taxes and penalties.

The Simple Fix

The system was not built to protect you here. Your provider will not remind you. The IRS will not warn you in advance.

The fix is 10 seconds per receipt:

- ●Get a medical receipt

- ●Take a photo with your phone

- ●Put it somewhere you will not lose it

A folder on your phone. Google Drive. A tool like Tripl that stores the receipt and tracks the expense automatically.

The people who leave their HSA invested for 20 years already do this. The delayed reimbursement strategy depends on receipts. So does the growth projection math that shows what your HSA could be worth over decades. Receipts are the foundation of every advanced HSA strategy.

Even if you never delay a reimbursement. Even if you swipe the card every single time. Save the receipt. Your provider is a bank. Banks do not do your taxes. The 10-second habit is the only HSA feature nobody sells you because nobody profits from it.

Frequently Asked Questions

Why does my HSA provider not just decline non-medical purchases?

HSA debit cards use merchant category codes to screen transactions. They decline at obviously non-medical merchants like clothing stores. But pharmacies and grocery stores with pharmacies sell both medical and non-medical items. The card sees the merchant category. It cannot see what is in your cart.

Does any HSA provider offer built-in receipt tracking?

A few. Lively and Fidelity have basic document storage. But these features are buried in settings and not actively promoted. They do not auto-match receipts to transactions or flag undocumented swipes.

What happens if my provider gets audited?

Provider audits cover financial reporting and compliance, not your individual spending. If the IRS audits your HSA distributions, they come to you. Your provider's role is confirming the distribution amounts they already reported on the 1099-SA.

Could the government require providers to track receipts in the future?

Possible. Legislation has been proposed. But as of 2026, there is no requirement for providers to verify or track the medical nature of distributions. The responsibility is the account holder's.

This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.