Your HSA Is Probably Losing Money

Not losing money in the stock market sense. Losing money to inflation while sitting in a cash account earning 0.01% APY.

The Employee Benefit Research Institute found that over 80% of HSA dollars sit in cash. Not invested. Not growing. Just sitting there, slowly losing purchasing power while inflation runs at 2% to 3% per year.

If your HSA balance is under $1,000, cash is fine. You might need it soon. But if you have $5,000 or more and you are not investing it, you are making an expensive mistake.

The Cost of Cash

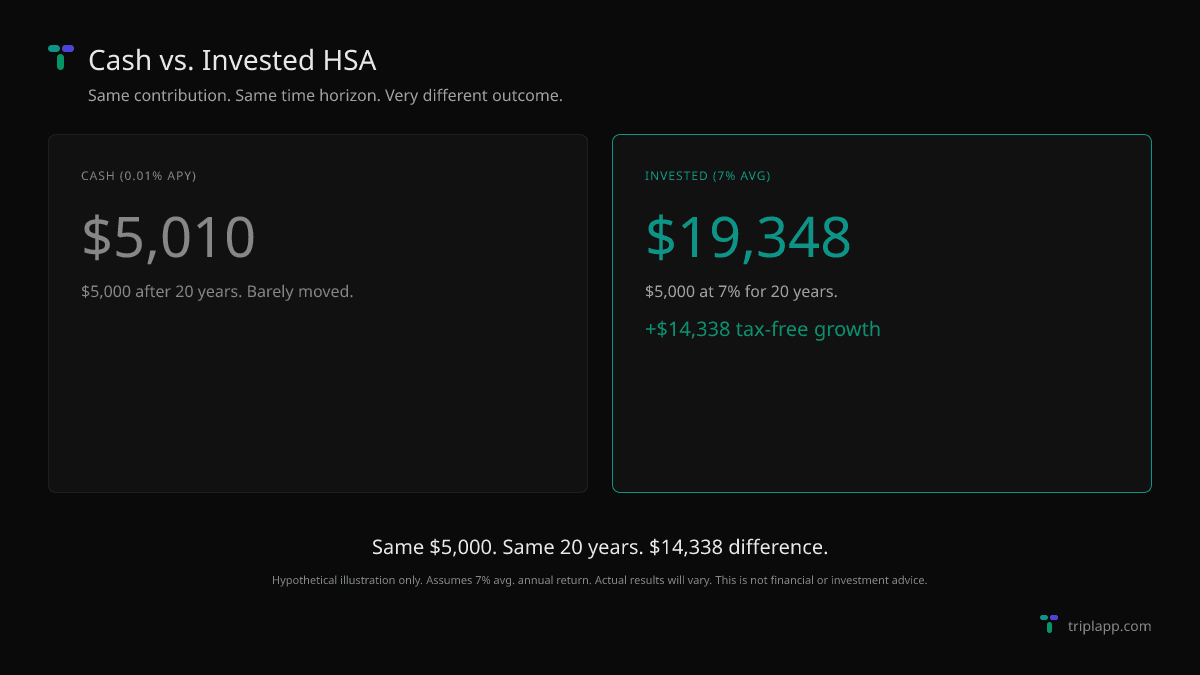

$5,000 sitting in HSA cash for 20 years at 0.01% APY grows to $5,010.

$5,000 invested in a broad stock index fund averaging 7% per year grows to $19,348.

That is $14,338 you left on the table. Tax-free dollars, gone because of a default setting you probably did not even know about.

Now scale that up. If you are maxing your HSA contributions at $4,400/year (individual) and keeping everything in cash:

| Time Period | Cash at 0.01% | Invested at 7% | Difference |

|---|---|---|---|

| 10 years | $44,004 | $63,390 | $19,386 |

| 20 years | $88,009 | $192,910 | $104,901 |

| 30 years | $132,013 | $444,695 | $312,682 |

*Hypothetical illustration. Assumes 7% avg. annual return. Actual investment returns will vary.*

Over 30 years, the difference is $312,682. That is the price of a default setting.

Three Approaches to HSA Investing

Approach 1: Keep It All in Cash

Who this is for: People who plan to use their HSA for current medical expenses and do not want any market risk.

The reality: This approach makes sense if you have high medical expenses and a low HSA balance. If you are spending most of what you contribute each year, investing is not practical.

But if you are healthy and building a balance, cash is the worst long-term option. Inflation eats 2% to 3% per year. Your 0.01% interest does not even come close.

When it works: HSA balance under $2,000. High current medical expenses. No emergency fund outside the HSA.

Approach 2: Target-Date Funds

Who this is for: People who want a simple, set-it-and-forget-it option.

Target-date funds automatically adjust their mix of stocks and bonds as you approach a target year. That is usually your expected retirement date. Pick the fund closest to when you turn 65, and it handles the rest.

The upside: Zero maintenance. Automatic rebalancing. Diversified across stocks and bonds.

The downside: Higher expense ratios than index funds. Typically 0.10% to 0.15% at low-cost providers, but some HSA platforms charge 0.30% or more. Also, the bond allocation starts earlier than most young savers need. If you are 30 years from retirement, a 10% to 20% bond allocation is just dragging down your returns.

Specific options:

- ●Fidelity Freedom Index funds (0.12% expense ratio)

- ●Schwab Target Index funds (0.08% expense ratio)

- ●Vanguard Target Retirement funds (0.08% expense ratio, available at some HSA providers)

Approach 3: Index Funds (DIY)

Who this is for: People comfortable choosing their own allocation who want the lowest cost and highest expected return.

This is the approach that most financial advisors recommend for long-term HSA investing. Pick a few low-cost index funds. Rebalance once a year. Done.

The upside: Lowest expense ratios (0.015% to 0.05%). Full control over your stock/bond split. No unnecessary bond drag when you are young.

The downside: You have to choose your allocation and rebalance periodically. This takes maybe 30 minutes per year.

Specific options by provider:

Fidelity HSA:

- ●Fidelity Total Market Index (FSKAX), 0.015% expense ratio

- ●Fidelity International Index (FSPSX), 0.035% expense ratio

- ●Simple allocation: 80% FSKAX, 20% FSPSX

Schwab HSA:

- ●Schwab Total Stock Market Index (SWTSX), 0.03% expense ratio

- ●Schwab International Index (SWISX), 0.06% expense ratio

- ●Simple allocation: 80% SWTSX, 20% SWISX

HSA Bank (TD Ameritrade):

- ●Vanguard Total Stock Market ETF (VTI), 0.03% expense ratio

- ●Vanguard Total International ETF (VXUS), 0.07% expense ratio

- ●Simple allocation: 80% VTI, 20% VXUS

The Cash Buffer Strategy

Here is the approach that balances safety and growth. Keep a small cash buffer in your HSA for near-term expenses. Invest everything else.

How much cash to keep: 1 to 2 times your annual deductible. If your HDHP deductible is $1,700, keep $1,700 to $3,400 in cash. This covers a worst-case medical year without touching your investments.

Everything above that buffer goes into investments. When your balance grows from new contributions, invest the amount above your cash target each quarter.

This way you are never caught needing to sell investments during a market dip to pay a medical bill. And the rest of your money is working for you.

What About Market Crashes?

This is the fear that keeps most people in cash. "What if the market drops 30% right when I need the money?"

Three things to consider:

1. The cash buffer covers short-term needs. You are not selling investments to pay for today's copay. The buffer handles that.

2. The market has always recovered. The S&P 500 has recovered from every crash in history. The 2008 crash recovered in about 4 years. The 2020 crash recovered in 5 months. If your time horizon is 10 or more years, temporary drops do not matter.

3. Time in the market beats timing the market. Missing just the 10 best trading days over a 20-year period cuts your returns nearly in half. The cost of staying in cash waiting for the "right time" is almost always higher. A temporary dip costs less than years of missed growth.

Picking the Right Provider

Not all HSA providers offer good investment options. Some charge monthly fees, have high investment minimums, or offer only expensive funds.

The best HSA providers for investing share three traits:

- ●No monthly maintenance fees (or fees waived above a low balance)

- ●Low-cost index fund options (expense ratios under 0.10%)

- ●Low or no minimum balance to start investing

If your employer's HSA provider has bad investment options, you can transfer your balance to a different provider. It takes a few weeks and some paperwork, but it is worth it if your current provider charges 0.50% expense ratios on their funds.

The One Mistake to Avoid

Do not treat your HSA like a checking account. The average HSA balance in America is under $4,000. That tells you most people are depositing money and spending it the same year.

An HSA used as a spending account saves you maybe 25% on medical expenses (your tax rate). An HSA invested for 20 years and used with the delayed reimbursement strategy can turn $4,400/year into nearly $200,000. The difference between those two outcomes is not income or luck. It is knowing which button to press in your HSA provider's dashboard.

Frequently Asked Questions

Do I have to invest my HSA with my current provider?

No. You can transfer your HSA balance to any provider that accepts transfers. The process takes 2 to 4 weeks. Your employer's contributions will still go to the original provider, but you can transfer periodically.

What is the minimum balance to start investing?

It varies by provider. Fidelity has no minimum. Some providers require $1,000 or $2,000 in cash before you can invest. Check your provider's rules.

Are HSA investments taxed?

No. That is the whole point. Dividends, capital gains, interest. All tax-free inside your HSA. This is the same treatment as a Roth IRA, except you also got a tax deduction on the contributions.

Should I invest more aggressively in my HSA than my 401(k)?

Many financial planners say yes. HSA withdrawals for medical expenses are tax-free at any age. Medical expenses are essentially guaranteed in retirement. The money will get used. A higher stock allocation means more growth on money you will almost certainly spend tax-free.

*This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.*