The Best-Kept Secret in Personal Finance

There is an HSA strategy so powerful that financial planners love it. They call it one of the best legal tax moves available to Americans. It is simple, completely IRS-approved, and yet most HSA holders have never heard of it.

Here is the core idea: pay out of pocket instead of using your HSA debit card. Save the receipt and let your HSA money stay invested. Then, months or years or even decades later, reimburse yourself tax-free.

The result? Your money grows tax-free inside the HSA for as long as you want, and you still get the tax-free withdrawal whenever you are ready.

How the Reimbursement Strategy Works

The IRS has a surprisingly generous rule: there is no time limit on HSA reimbursements. The expense must occur after you opened your HSA. After that, you can reimburse yourself at any point in the future. The relevant IRS guidance is in Publication 969.

Here is the step-by-step process:

Step 1: You have a qualified medical expense, say a $200 doctor visit.

Step 2: Instead of paying with your HSA debit card, you pay with your regular credit card or checking account.

Step 3: You save the receipt (digitally is fine, a photo or PDF works).

Step 4: Your $200 stays in your HSA, invested in index funds, growing tax-free.

Step 5: Whenever you want (next month, next year, or twenty years from now) you withdraw $200 from your HSA as a reimbursement. Completely tax-free.

The magic is in Step 4. That $200 is not sitting idle. It is growing. At a 7% average annual return, that $200 becomes $387 in 10 years and $773 in 20 years, all tax-free.

A Real-World Example

Let us say you are 30 years old and you have $3,000 in annual medical expenses. You have the cash flow to pay these out of pocket. Here is what happens if you use the reimbursement strategy versus paying directly from your HSA:

Scenario A: Pay Directly from HSA

- ●You spend $3,000 per year from your HSA on medical bills

- ●Your HSA balance stays relatively flat (contributions minus spending)

- ●At age 55, your HSA has whatever you have contributed minus what you have spent

Scenario B: Pay Out of Pocket, Reimburse Later

- ●You pay $3,000 per year out of pocket and keep receipts

- ●Your full HSA contributions stay invested and grow at 7% annually

- ●After 25 years, your HSA has grown significantly

- ●You have accumulated $75,000 in reimbursable receipts

- ●You can withdraw $75,000 completely tax-free at any time

- ●The remaining balance continues to grow tax-free

Over 25 years, the difference in your HSA balance could be over $100,000. That is purely from letting the money grow instead of spending it immediately. And every dollar of your accumulated receipts can be withdrawn tax-free whenever you need it.

Why This Is Completely Legal

Some people hear about this strategy and think it sounds too good to be true. But the IRS has explicitly confirmed that there is no deadline for reimbursement. Here are the key rules:

- ●The expense must be qualified. It must be a legitimate medical expense as defined under IRS Section 213(d). See our complete list of HSA-eligible expenses for details.

- ●The expense must occur after the HSA was established. You cannot reimburse yourself for expenses that happened before you opened your HSA.

- ●You must keep records. The IRS requires that you maintain records sufficient to show that the distributions were for qualified medical expenses. Keep your receipts.

- ●There is no time limit. The IRS does not impose a deadline for when you must take the reimbursement.

This is not a loophole or a gray area. It is the intended design of the HSA. Congress created HSAs to encourage people to save for healthcare costs, and the open-ended reimbursement window is a deliberate feature.

The Critical Requirement: Keep Your Receipts

This entire strategy falls apart without documentation. If the IRS ever asks you to prove that your HSA withdrawals were for qualified expenses, you need receipts. Here is how to build a bulletproof system:

Digital is best. Take a photo of every medical receipt or save the PDF from your insurance company's explanation of benefits (EOB). Store them in a dedicated folder in your cloud storage.

Track the details. For each expense, record the date, the provider, the amount, and a brief description of the service.

Keep insurance EOBs. Your insurance company's explanation of benefits is excellent documentation because it shows what you paid after insurance.

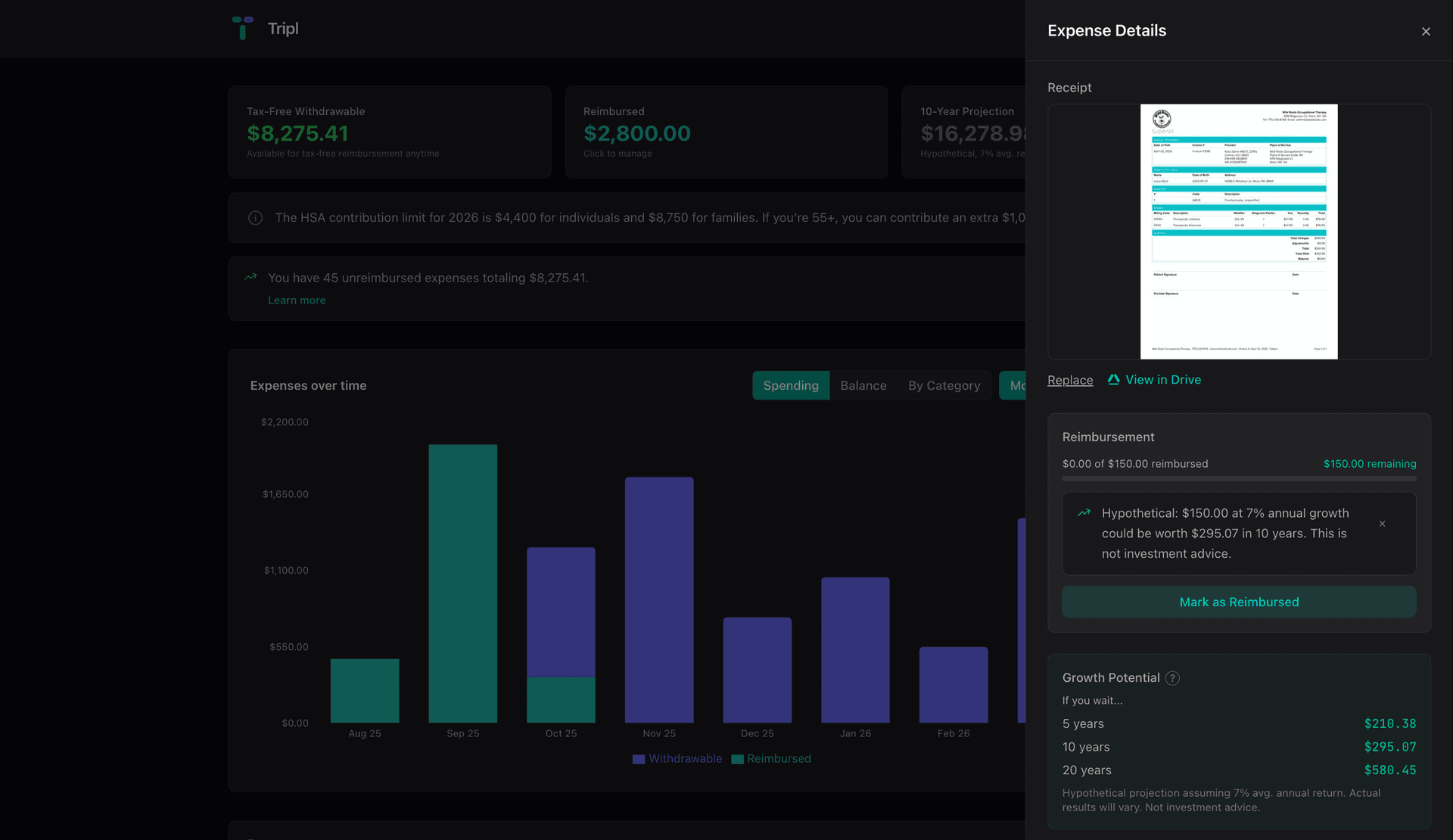

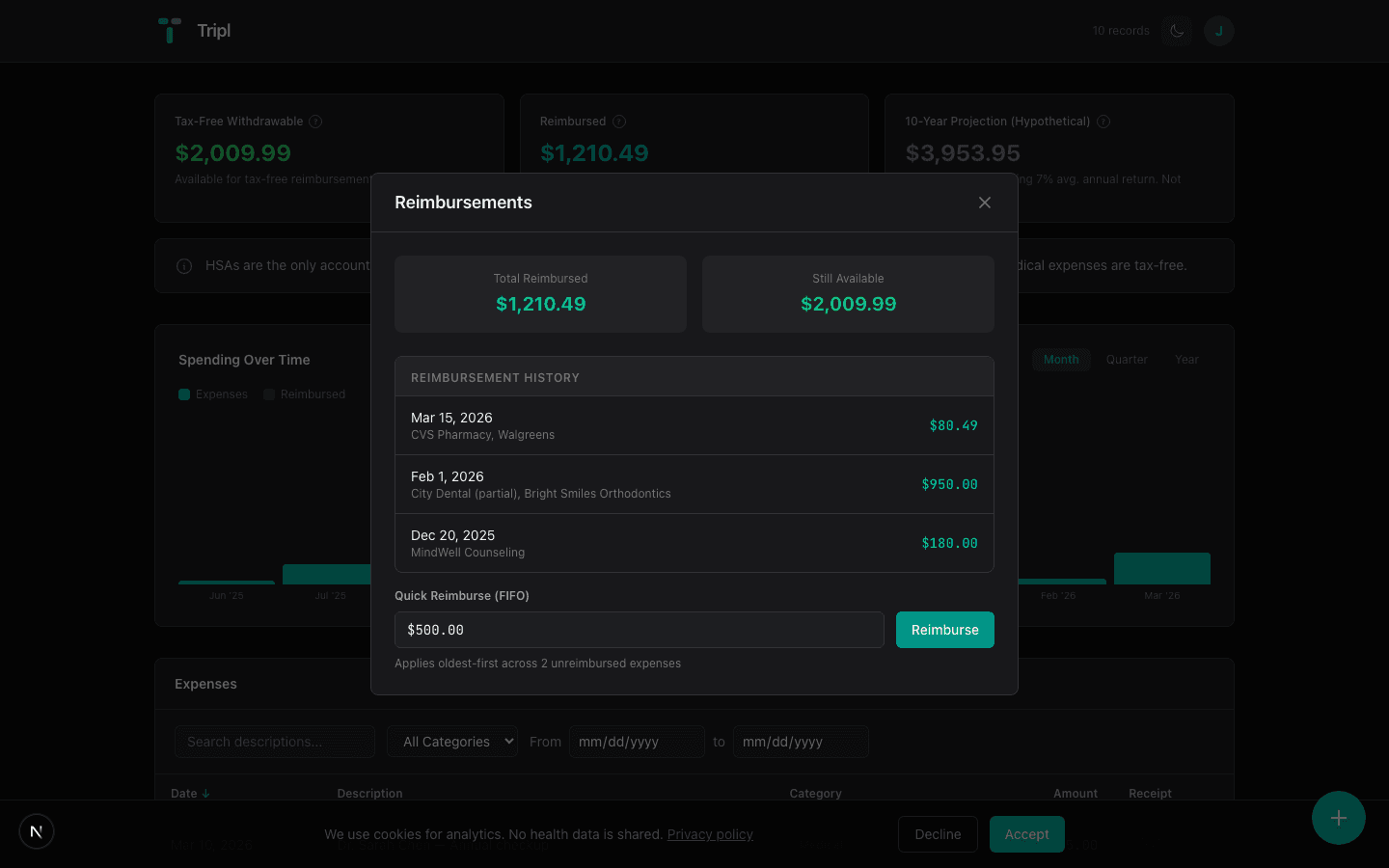

Use a tracking tool. A spreadsheet works, or you can use a dedicated HSA receipt tracker to automatically total your reimbursable amount over time. This is exactly what Tripl is built to do. It tracks your HSA receipts so you always know your total reimbursable amount.

When to Actually Reimburse Yourself

The beauty of this strategy is flexibility. Here are common scenarios when people choose to reimburse:

- ●Emergency fund backup: If you face an unexpected expense, your accumulated HSA receipts function as a tax-free emergency fund.

- ●Job loss or career change: If your income drops, you can reimburse yourself to supplement your cash flow without any tax consequences.

- ●Retirement: Withdraw against decades of accumulated receipts for tax-free income in retirement.

- ●Large purchase: Need a down payment for a house? If you have enough accumulated receipts, you can pull the money tax-free.

The key insight is that your HSA receipts give you optionality. You are not locked into a specific withdrawal timeline. You decide when and how much to reimburse based on your life circumstances.

Combining With the Triple Tax Advantage

The reimbursement strategy amplifies the HSA's triple tax advantage. Here is the full picture:

- ●Tax-free contributions: You contribute pre-tax dollars to your HSA, reducing your taxable income.

- ●Tax-free growth: Your contributions are invested and grow without being taxed on capital gains or dividends.

- ●Tax-free withdrawals: When you eventually reimburse yourself, the withdrawal is completely tax-free.

No other account in the U.S. tax code can match this. A 401(k) gives you #1 and #2 but not #3. A Roth IRA gives you #2 and #3 but not #1. Only the HSA delivers all three.

Common Mistakes to Avoid

Do not lose your receipts. This is the number one risk. Without documentation, you cannot prove your withdrawals were for qualified expenses.

Do not reimburse expenses that occurred before your HSA was opened. The IRS is clear on this: the expense must happen after you establish the account.

Do not forget to actually invest. Many HSA providers keep your balance in a low-interest cash account by default. You need to actively choose investments (typically low-cost index funds) to get the growth that makes this strategy worthwhile.

Do not use your HSA debit card for expenses you plan to reimburse later. If you swipe the card, the money leaves your HSA immediately. Pay with a different payment method and save the receipt.

Getting Started Today

You do not need a lot of money to begin. Here is how to start:

- ●Make sure your HSA balance is invested. Move your balance into index funds, keeping only a small cash buffer for any near-term expenses you cannot cover out of pocket.

- ●Start paying medical expenses out of pocket. Use your regular credit card or bank account for doctor visits, prescriptions, and other qualified expenses.

- ●Save every receipt. Build the habit now. Even small expenses add up over years.

- ●Track your running total. Know how much you have in reimbursable receipts at all times. This is your tax-free withdrawal capacity.

- ●Be patient. The power of this strategy comes from time. The longer your money grows tax-free, the larger the benefit.

The HSA reimbursement trick is not complicated. It just requires a small change in habit: pay with your regular card instead of your HSA card, and save the receipt. That simple shift can be worth tens of thousands of dollars over your lifetime.

Track the Strategy

The reimbursement trick only works if you save every receipt. Tripl stores each one, tracks your reimbursable total, and keeps a full record of what you have claimed. It also shows growth projections so you can decide when to reimburse.

*This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.*