The Swipe You Do Not Think About

Your HSA debit card feels like free money. You paid with pre-tax dollars. You saved on taxes. Good job.

But every swipe pulls money out of an investment account that could be growing tax-free for decades. That $150 copay is not just $150. It is whatever that $150 would have become if you left it alone.

This is not about guilt. It is about knowing the real price of convenience so you can make an informed choice.

The Math Behind a Single Swipe

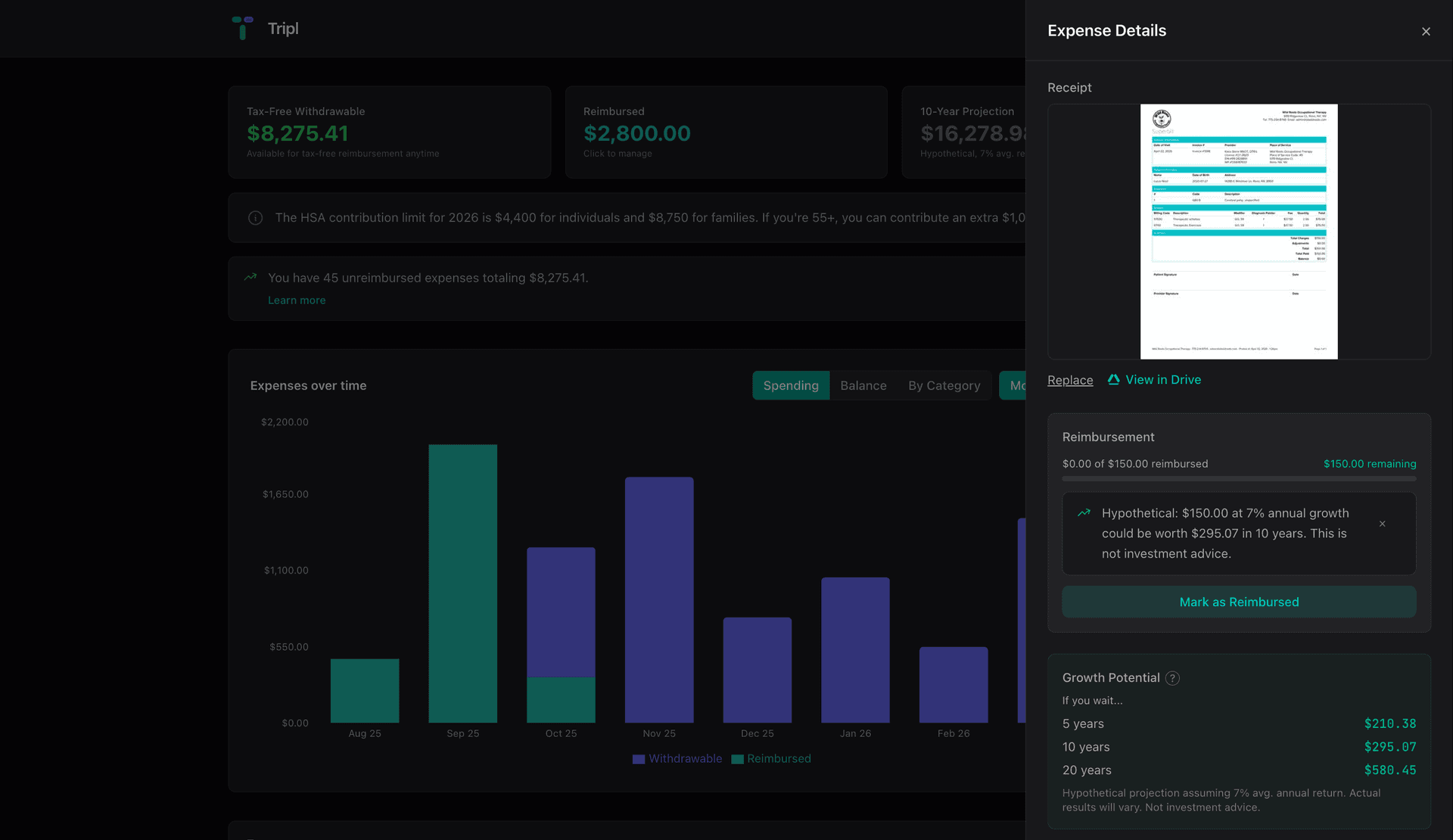

A $150 copay swiped from your HSA today. Here is what that $150 would be worth if you paid out of pocket instead. Let the HSA grow.

| Years Invested | Value at 7% Return | What You Gave Up |

|---|---|---|

| 5 years | $210 | $60 |

| 10 years | $295 | $145 |

| 20 years | $580 | $430 |

| 30 years | $1,142 | $992 |

*Hypothetical illustration. Assumes 7% avg. annual return. Actual investment returns will vary.*

One swipe. One copay. $992 gone over 30 years. That $150 was already pre-tax money. The true cost is even higher because you also lost the tax-free growth.

Three Real Scenarios

Let us look at what different levels of annual HSA spending look like over time. These assume you are currently swiping your HSA card for everything and could instead be paying out of pocket.

Scenario 1: $1,000/year in HSA spending

You are relatively healthy. A few copays, some prescriptions, maybe a dental visit.

| Time Period | Money Swiped | Value If Invested Instead |

|---|---|---|

| 10 years | $10,000 | $14,784 |

| 20 years | $20,000 | $43,865 |

| 30 years | $30,000 | $101,073 |

*Hypothetical illustration. Assumes 7% avg. annual return. Actual investment returns will vary.*

You gave up $71,073 in tax-free growth over 30 years. That is not nothing.

Scenario 2: $3,000/year in HSA spending

A family with regular medical expenses. Kids, prescriptions, a few specialist visits.

| Time Period | Money Swiped | Value If Invested Instead |

|---|---|---|

| 10 years | $30,000 | $44,352 |

| 20 years | $60,000 | $131,596 |

| 30 years | $90,000 | $303,219 |

*Hypothetical illustration. Assumes 7% avg. annual return. Actual investment returns will vary.*

$213,219 in lost growth. That is a down payment on a house. Tax-free.

Scenario 3: $5,000/year in HSA spending

A family with braces, contacts, regular therapy, and a few bigger bills.

| Time Period | Money Swiped | Value If Invested Instead |

|---|---|---|

| 10 years | $50,000 | $73,918 |

| 20 years | $100,000 | $219,326 |

| 30 years | $150,000 | $505,365 |

*Hypothetical illustration. Assumes 7% avg. annual return. Actual investment returns will vary.*

Half a million dollars. From expenses you were going to have anyway. The only difference is which card you pulled out of your wallet.

When Swiping Makes Total Sense

This is not a purity test. There are plenty of times when using your HSA debit card is the right move.

You do not have the cash. If paying a $2,000 ER bill out of pocket means missing rent, swipe the card. Financial stress is a real cost too. Your HSA exists for moments like this.

The expense is huge and unexpected. A $5,000 surgery or $3,000 dental bill when you are already stretched. Nobody should go into credit card debt at 24% APR to "save" money in their HSA.

You are close to retirement. If you are 60 and plan to use the money at 65 anyway, the growth window is short. Five years of growth on $500 is about $200. That might not be worth the hassle of tracking receipts.

You have not built the habit yet. Switching from swiping to saving receipts takes time. Start small. Pay one copay out of pocket this month. Save the receipt. See how it feels. You can always reimburse yourself later if you change your mind.

The Simple Habit Shift

The delayed reimbursement strategy works like this:

- ●Go to the doctor

- ●Pay with your regular credit card (earn points while you are at it)

- ●Save the receipt

- ●Let your HSA stay invested

- ●Reimburse yourself whenever you want. Tomorrow, next year, or in 20 years.

Same purchase. Same tax benefit. Different timing. That timing difference is worth tens of thousands of dollars.

The receipt is the key. Without it, you cannot reimburse yourself later. A photo on your phone works. A PDF from your insurance company works. A shoebox full of paper works, but a digital backup is smarter.

Tools like Tripl make this easy. Upload the receipt, track the expense, reimburse when you are ready. But even a folder in Google Drive gets the job done.

The Credit Card Bonus

Here is a detail most people miss. When you pay with your HSA debit card, you earn zero credit card rewards.

Pay with your regular credit card and save the receipt. You earn 1% to 2% cash back (or points). On $3,000/year in medical expenses, that is $30 to $60 in free rewards. Not life-changing, but it adds up. And you still get the full HSA tax benefit when you reimburse yourself.

What the Numbers Actually Mean

Say you are 30, spending $3,000/year on medical expenses. Make this one change and you are looking at roughly $200,000 more in your HSA by 60.

You did not earn more money. You did not cut spending. You did not change your medical care. You just pulled a different card out of your wallet and saved a receipt.

That is the real cost of convenience. Not the $3,000 you swiped this year. The $200,000 you never had because you did not know the card mattered.

There are seven common HSA mistakes that cost people money. Using the debit card by default is one of the biggest.

Frequently Asked Questions

Can I reimburse myself for expenses from years ago?

Yes. The IRS has no time limit on HSA reimbursements. You can reimburse yourself for any qualified medical expense that occurred after your HSA was opened. There is no time limit. The only requirement is documentation.

Do I need to keep the original receipt?

The IRS accepts digital copies. A photo of your receipt, a PDF from your insurance portal, or an explanation of benefits (EOB) all work. Store them somewhere you will not lose them.

What if I reimburse myself and then get audited?

You need to show the expense was for a qualified medical purpose. It also must have occurred after your HSA was established. Keep the receipt, the date of service, the provider name, and the amount. That is all the IRS needs.

Is there a minimum amount worth tracking?

No official minimum. But practically, tracking a $15 copay is worth it if you are building the habit. Over 30 years of quarterly copays, those $15 charges add up to thousands in potential tax-free growth.

See What Each Swipe Costs

Tripl tracks every HSA expense and keeps a full reimbursement record. For unreimbursed expenses, it shows growth projections. See what that $150 copay would be worth in 10 or 20 years. The math makes the decision easier.

*This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.*