Updated April 13, 2026. Tax deadline is April 15.

The Form Every HSA Holder Has to File

If you have a Health Savings Account, you file Form 8889 every year. No exceptions. Even if you did not contribute a single dollar. Even if you did not spend a single dollar. If the account exists, the form is required.

Most tax software handles it automatically. But "automatically" does not mean "correctly." The IRS gets a copy of your 1099-SA and 5498-SA from your HSA provider. If your Form 8889 does not match, you will hear from them.

Here is how the form works, section by section.

Part I: HSA Contributions and Deduction (Lines 1 through 13)

This section calculates your HSA tax deduction.

Line 2 is contributions you made outside of payroll. Direct deposits, transfers, catch-up contributions. If your contributions come out of your paycheck pre-tax, those are reported on Line 9 with employer contributions (check your W-2 Box 12, Code W). For 2025 tax returns (filed in 2026), the total limits are $4,300 individual and $8,550 family.

Line 6 is your annual contribution limit. This is where part-year eligibility gets tricky.

Line 9 is your employer contributions. This is the number people forget most often. Your W-2 Box 12, Code W includes both your payroll deductions AND your employer's contributions. You need to split them correctly.

Here is the math. Box 12 Code W shows $5,000. Your employer contributed $1,000. Your payroll deductions were $4,000. Line 9 gets $5,000 (the full Box 12 amount). Line 2 gets $0, because payroll deductions are already captured in Box 12. If you also made a direct contribution outside payroll of $300, Line 2 gets $300.

Line 13 is your HSA deduction. This flows to Schedule 1 of your 1040, reducing your adjusted gross income.

Part II: HSA Distributions (Lines 14a through 17c)

This section reports what you took out.

Line 14a is your total distributions for the year. Your HSA provider sends this on Form 1099-SA.

Line 14b is rollover contributions. If you moved money between HSA providers, report it here.

Line 14c is excess contributions you removed. If you over-contributed and withdrew the excess before the tax deadline, it goes here.

Line 15 is your qualified medical expenses paid with HSA funds. This is the number that determines whether you owe extra tax.

If Line 15 is less than Line 14a, the difference is a non-qualified distribution. You will owe income tax on it. If you are under 65, you also owe the 20% penalty (Line 17b).

Part III: Income and Additional Tax for Failure to Maintain HDHP Coverage (Line 18 through 21)

This section only applies if you used the "last-month rule." The last-month rule lets you contribute the full annual limit even if you only had HSA-eligible coverage on December 1. But there is a catch: you must maintain coverage through December 31 of the following year.

If you used the last-month rule in the prior year and then lost your HDHP coverage, Part III kicks in. It calculates the extra income and 10% penalty you owe.

Most people never touch Part III. But if you switched from an HDHP to a PPO mid-year after using the last-month rule, this is where it hits you.

The Last-Month Rule: A Deeper Look

The last-month rule is powerful but risky. If you are HSA-eligible on December 1, the IRS lets you contribute as if you were eligible all year.

Say you started a new job in November and enrolled in an HDHP. You are only covered for 2 months. Normally, you would prorate: 2/12 of the annual limit. With the last-month rule, you get the full $4,300.

The catch: you must keep HDHP coverage through December 31 of the following year. If you break coverage during that "testing period," you owe income tax plus a 10% penalty on the excess. Not 20%. This is a different penalty from the non-medical distribution penalty.

Five Mistakes That Trigger IRS Letters

1. Forgetting employer contributions. Your employer's HSA contributions count toward your annual limit. If your employer puts in $1,500 and you contribute $4,300, your total is $5,800. The 2025 individual limit is $4,300. You are $1,500 over. You need to remove the excess before the tax filing deadline. Otherwise you pay a 6% excise tax every year it sits there.

2. Double-counting payroll contributions. Your W-2 Box 12 Code W includes payroll deductions. Do not also report them on Line 2 of Form 8889. That double-counts them. Line 2 is only for contributions made outside of payroll.

3. Missing the proration. If you had HDHP coverage for only 8 months, your contribution limit is 8/12 of the annual max. Unless you used the last-month rule. Forgetting to prorate is one of the most common errors.

4. Not filing Form 8889 at all. Some people with HSAs assume their tax software handles everything. If you use a very basic filing tool, it might skip Form 8889 entirely. The IRS knows you have an HSA (your provider reports it). If you do not file the form, they will send a notice.

5. Reporting non-qualified distributions incorrectly. If you used HSA money for non-medical expenses, you owe income tax and the 20% penalty (if under 65). Some people forget to report the distribution or misclassify it as qualified. Your 1099-SA does not distinguish between qualified and non-qualified. That is your job on Form 8889.

California and New Jersey: The Extra Step

If you live in California or New Jersey, your state does not recognize the HSA tax deduction. You need to add back your HSA contributions on your state return.

We covered this in detail in our California and New Jersey HSA state taxes guide. The short version: you still get the federal deduction, but your state will tax contributions and earnings. Keep separate records.

How Form 8889 Connects to Your 1040

Here is the flow:

- ●Form 8889 Part I calculates your HSA deduction

- ●That deduction flows to Schedule 1, Line 13 of your 1040

- ●Schedule 1 flows to 1040, Line 10 (adjustments to income)

- ●This reduces your adjusted gross income (AGI)

Your AGI affects dozens of other tax calculations. Student loan interest phaseouts, Roth IRA contribution limits, child tax credit phaseouts, premium tax credits. Lowering your AGI with HSA contributions creates downstream savings beyond just the deduction itself.

The Contribution Deadline

You have until the tax filing deadline (April 15, 2026 for 2025 contributions) to make HSA contributions for the prior year. This means you can contribute to your HSA in January through April 2026 and apply it to your 2025 return.

This is the same rule as IRA contributions. If you have not maxed out your 2025 HSA and you are filing in March, you can still contribute the difference before April 15. Your HSA provider will ask which tax year the contribution applies to. Make sure you pick the right one.

The Bottom Line

Form 8889 is not complicated. It is three sections. Contributions, distributions, and the testing period. The problems come from small errors. Double-counting payroll contributions. Forgetting employer money counts toward the limit. Not prorating for partial-year coverage.

Get the contribution limits right, match your numbers to your 1099-SA and W-2 Box 12, and you are done.

Frequently Asked Questions

Do I need to file Form 8889 if I did not contribute to my HSA this year?

Yes. If you have an HSA, you must file Form 8889 with your tax return every year. Even if you made no contributions and took no distributions, the IRS expects the form. Your HSA provider reports your account to the IRS regardless.

What happens if I over-contributed to my HSA?

Remove the excess contribution (plus any earnings on it) before your tax filing deadline. If you miss the deadline, you owe a 6% excise tax on the excess. It applies every year the excess remains in the account. Your HSA provider can process an "excess contribution removal."

Can I file Form 8889 if I use free tax software?

Some free filing tools support Form 8889 and some do not. TurboFree and FreeTaxUSA typically support it. If your software does not generate Form 8889 automatically, you may need to upgrade or file it manually.

My spouse and I both have HSAs. Do we each file a separate Form 8889?

Yes. Each spouse with an HSA files their own Form 8889. If you file jointly, both forms attach to the same return. Your combined contributions cannot exceed the family limit ($8,550 for 2025).

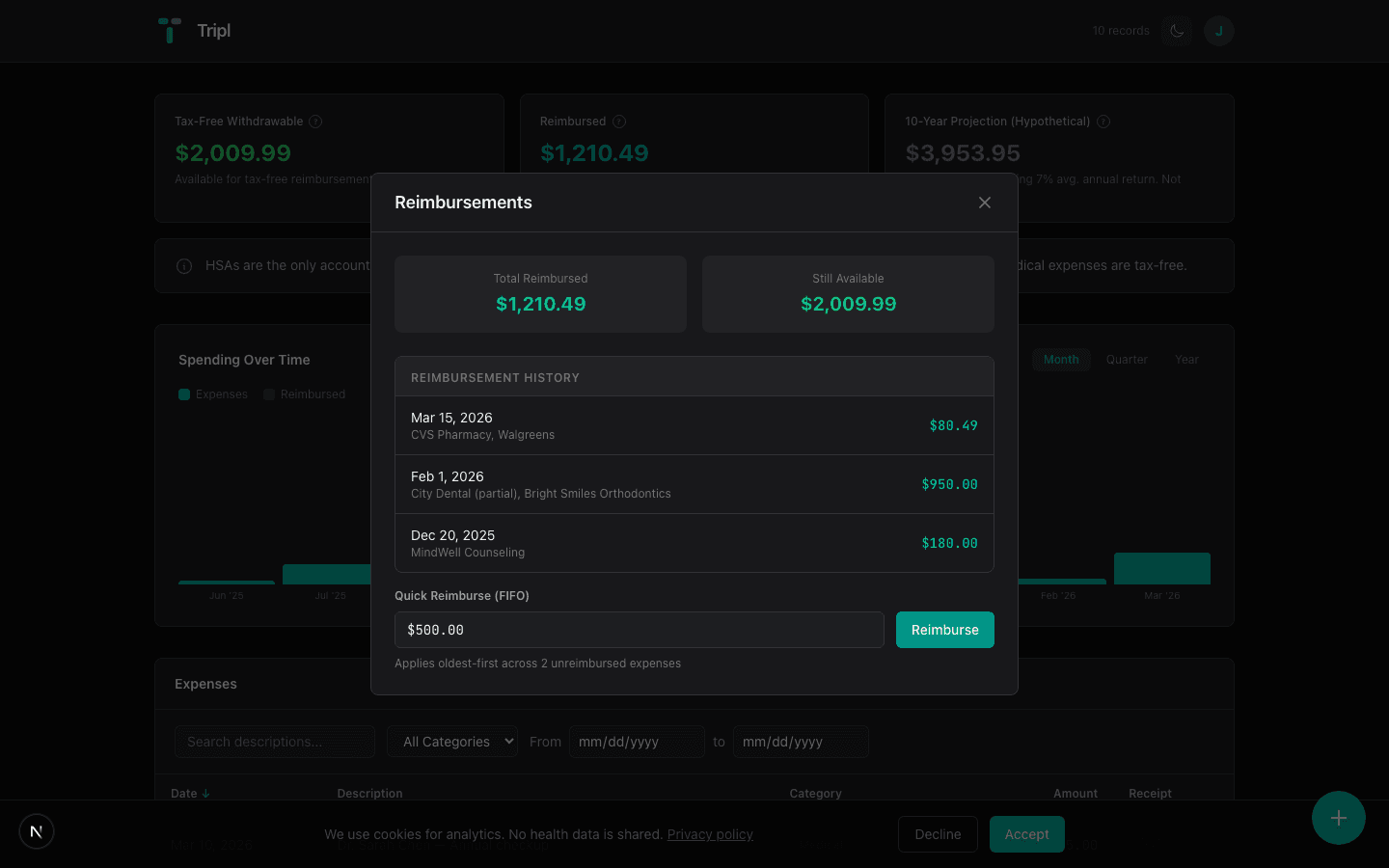

Pull Your Line 15 Number in Tripl

If you tracked receipts in Tripl this year, you already have your Part II Line 15 number.

- ●Log in at triplapp.com

- ●Open Reimbursements on the dashboard

- ●Click Export Report

The PDF shows every reimbursed expense with the date, amount, and category. Match the total to your 1099-SA and you are done. Takes about 8 seconds.

If you did not track receipts this year, start now. Every receipt you save today is one less thing to dig up next April.

*This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.*