The Bills Start Before the Baby Gets Home

If you recently had a baby or you are expecting, let me save you some stress. Your HSA is about to become your favorite financial tool, and not just for the obvious reasons.

I remember looking at the first hospital bill after my kid was born. The delivery, the epidural, the overnight stay, the pediatrician's visit on day one. It was a wall of charges. But here is the thing: almost every single line item was HSA-eligible.

Everything That Counts in Year One

You probably know doctor visits and hospital bills qualify. But here is the full picture for that first year:

Pregnancy and delivery:

- ●All prenatal visits and ultrasounds

- ●Hospital delivery costs (vaginal or C-section)

- ●Epidural and anesthesia fees

- ●Lab work and blood tests

- ●Postpartum checkups

Baby's medical care:

- ●Pediatrician well-baby visits

- ●Vaccinations

- ●Circumcision (if applicable)

- ●Any specialist referrals

The stuff people forget about:

- ●Breast pump and supplies

- ●Lactation consultant visits

- ●Infant pain relievers (Tylenol, gas drops)

- ●Diaper rash cream (yes, really)

- ●Saline drops for stuffy noses

- ●Baby sunscreen (SPF 15+)

- ●Prenatal vitamins (if prescribed)

- ●Postpartum mental health visits

That last one is important. Postpartum depression and anxiety are real, and therapy or psychiatry visits are fully HSA-eligible. Do not skip care because you are unsure if it is covered. It is. For a full breakdown of every category, see the complete HSA-eligible expenses list.

Switch to Family Coverage

This one catches people off guard. If you had individual HSA coverage before the baby, switch to family coverage. You have a qualifying life event window to make the change. For 2026, that bumps your contribution limit from $4,400 to $8,750. Almost double.

Most employers give you 30 days from the birth to make the change. Do not let this window close.

The Big Decision: HSA Card or Out of Pocket?

A delivery can cost $2,000 to $5,000 after insurance. You have two options:

Option 1: Swipe the HSA debit card. Easy, painless, money is gone.

Option 2: Pay out of pocket, save every receipt, and let that money keep growing in your HSA.

If you can swing it financially, option 2 wins by a lot. A $4,000 delivery bill left invested at 7% becomes $7,869 in 10 years and $15,478 in 20 years. All of that is tax-free when you eventually reimburse yourself.

But if cash is tight with a newborn (and it usually is), pay from your HSA. Zero shame in that. That is literally what it is there for.

One Habit to Start Now

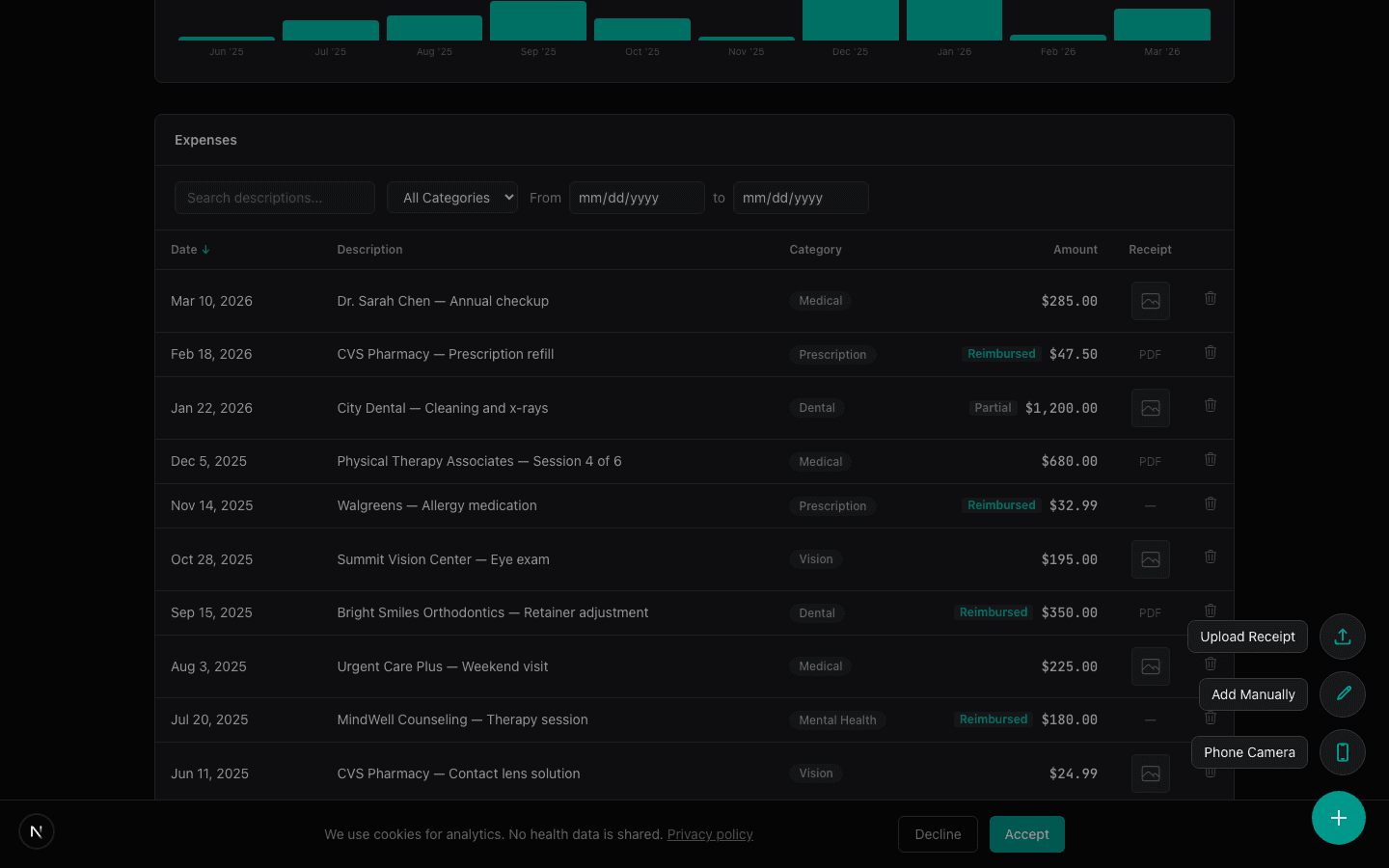

Save every medical receipt from day one. Every copay, every pharmacy run, every tube of diaper rash cream. Use your phone to snap a photo right there in the parking lot. It takes five seconds.

Those small purchases add up fast in year one. A $15 copay here, a $30 prescription there. Over 12 months it can easily total $2,000 to $3,000 in trackable expenses on top of the delivery itself.

Your future self will thank you when that stack of receipts turns into a tax-free withdrawal years down the road.

Track Year One in One Place

The first year with a new baby generates thousands in HSA-eligible expenses. Delivery, copays, prescriptions, diaper rash cream. It is easy to lose track. Tripl stores every receipt, parses it automatically, and keeps your reimbursement records in one place. You always know your total, and the records are there when tax season comes.

*This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.*