The Most Common Question I Get About Tripl

"I use the debit card. Why would I need receipts?"

I hear some version of this every week. It makes perfect sense. You swipe at CVS for your kid's amoxicillin. You swipe at the pediatrician for the copay. The transaction clears. You move on with your day.

But your card statement shows "CVS Pharmacy, $47.63." It does not show the breakdown. $12 for an antibiotic, $23 for an allergy refill, $12.63 for diaper rash cream. All three are qualified. But the bank statement cannot prove that.

I learned this while researching IRS rules for Tripl. It surprised me more than anything else I found.

The Short Answer

Yes. You need receipts even if you use the debit card.

The debit card moves money from your HSA to the store. That is all it does. It does not create a record of what you bought.

The IRS needs two things for every HSA distribution. First, that the money went to a medical expense. Second, that the expense was "qualified" under their rules. Your card statement proves neither.

What Actually Counts as Proof

The IRS wants three details for every HSA purchase.

| What the IRS Needs | What Your Card Statement Shows |

|---|---|

| Date of service or purchase | Yes |

| Amount paid | Yes |

| What the expense was for | No |

Date of service or purchase

- What Your Card Statement Shows

- Yes

Amount paid

- What Your Card Statement Shows

- Yes

What the expense was for

- What Your Card Statement Shows

- No

That third column is the gap. A pharmacy receipt shows "Amoxicillin, 30 tablets, $12." A card statement shows "CVS Pharmacy, $12." One proves a qualified medical expense. The other proves you went to CVS.

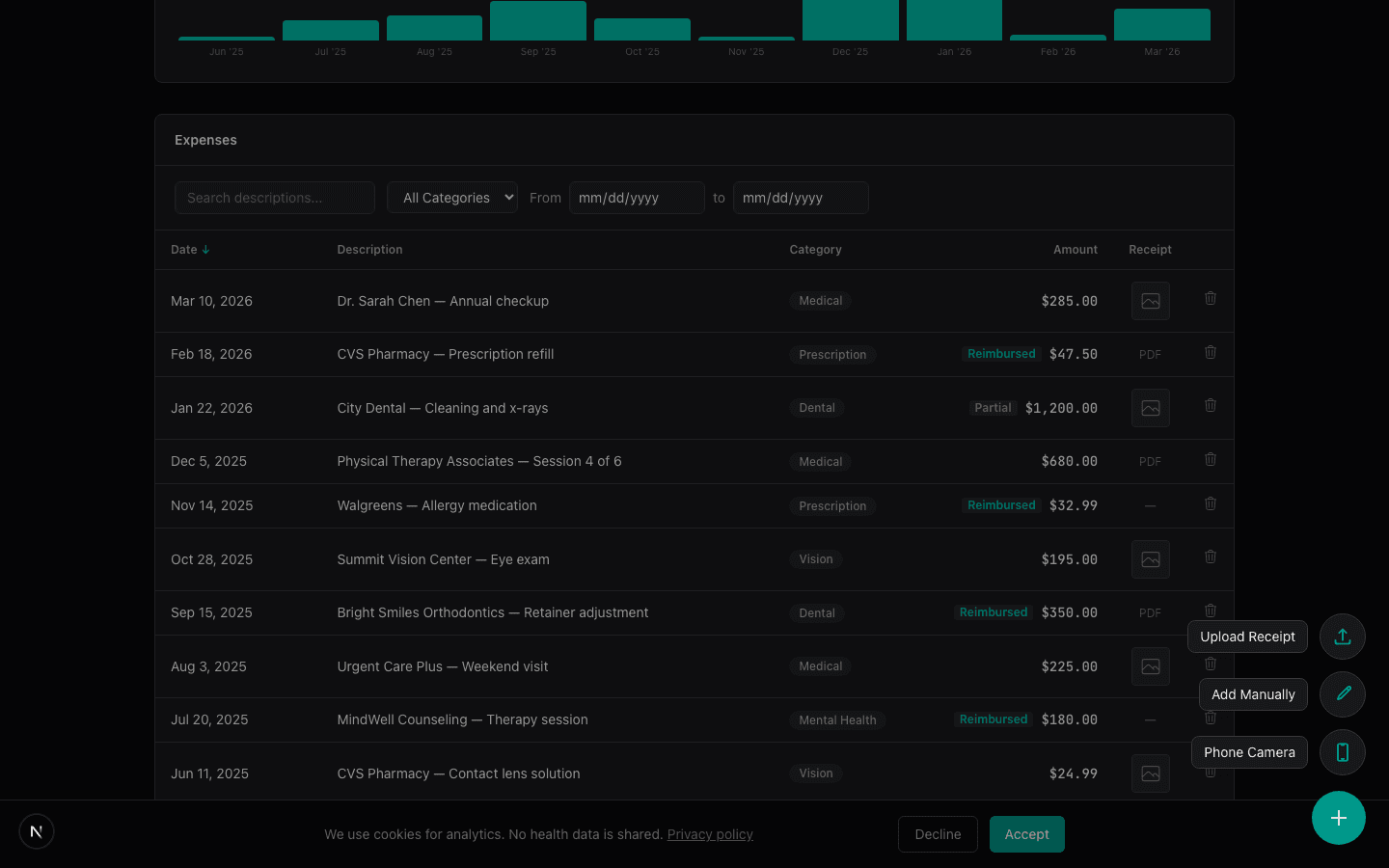

The IRS accepts several forms of documentation. A store receipt works. A pharmacy printout works. An explanation of benefits (EOB) from your insurance works. An itemized bill from your doctor works. Even a phone photo of any of these works.

What does not work: your HSA provider's transaction log showing "CVS, $47.63."

What Your HSA Provider Does and Does Not Do

Your HSA provider reports one number to the IRS each year. Total distributions. That is it. It shows up on the 1099-SA.

One number. No line items. No categories. No proof of what any of the money went to.

Your provider does not ask what you bought at CVS. They do not match swipes to medical expenses. They do not store receipts. They are a bank. They hold money and move money. The record-keeping is on you.

This is actually why I built Tripl. The card creates a payment trail. Not a medical trail. Those are very different things. And there was no simple tool to close that gap.

How Far Back Can the IRS Look?

Seven years. In cases of suspected fraud, there is no time limit.

Most HSA holders will never be audited. But "probably fine" is not a plan. The penalty for a distribution you cannot prove was qualified is steep. It becomes taxable income. If you are under 65, add a 20% penalty on top.

Here is what that looks like with real numbers. Say you have been swiping for 5 years at roughly $3,000 per year. That is $15,000 in distributions. If you get audited and cannot produce receipts:

| Item | Amount |

|---|---|

| Distributions reclassified as income | $15,000 |

| Federal income tax at 22% bracket | $3,300 |

| 20% additional penalty (under 65) | $3,000 |

| Total tax and penalty | $6,300 |

$6,300 because of missing pharmacy printouts. Actually, because of skipping a 10-second phone photo.

But Nobody Gets Audited for HSA, Right?

True for most people. HSA-specific audits are not common. The IRS has limited resources and tends to focus on larger accounts.

But "not common" is not "impossible." The IRS receives your 1099-SA. They also get your tax return. If the numbers look off, or if your distributions seem high relative to your income, it can trigger a review.

The scenario that should concern you more: your tax return gets audited for a completely different reason. The agent notices your HSA distributions while they are digging around. Now you need receipts for every swipe from the last 3 years.

The point is not to scare you. It is that saving a receipt takes 10 seconds and skipping it creates a risk that hangs around for 7 years.

The 10-Second Fix

Every time you pay for something medical, save the receipt. Phone photo, upload to an HSA receipt tracker or a Google Drive folder, done. The whole thing takes about 10 seconds.

Even a folder on your phone labeled "HSA Receipts" gets the job done. You do not need an app. You need the habit.

The people who use the delayed reimbursement strategy already do this. They pay out of pocket, save the receipt, let their HSA stay invested. The receipt is the whole foundation. Without it, you cannot reimburse yourself later and you cannot prove the expense if audited. One rule the strategy depends on: the expense has to be incurred after you opened the HSA. Bills from before the account existed never qualify.

Whether you swipe the card or pay out of pocket, the receipt matters. The card is not the record. The receipt is.

What if You Have Not Been Saving Receipts?

Start today. Here is the recovery playbook.

Check your pharmacy's online account. CVS and Walgreens keep 12 to 24 months of purchase history. Your doctor's office can reprint bills. Your insurance portal has EOBs going back several years. Search your email for "copay" and "payment confirmation." You will find more than you expect.

We wrote a full recovery guide for this exact situation: What if I Lose My HSA Receipts?

You will not recover everything. But anything you pull together is better than the alternative.

Common Questions

Does the HSA debit card transaction count as a receipt?

No. The transaction shows you paid a vendor on a certain date. It does not show what you bought. The IRS needs the "what," not just the "where."

What format do receipts need to be in?

The IRS accepts paper or digital. A phone photo is fine. A PDF from your insurance portal is fine. Just make sure it shows the date, provider, amount, and what the expense was for.

How long should I keep them?

At least 7 years from the distribution date. If you are using delayed reimbursement, keep them until you reimburse yourself plus 7 more years after that. Just keep everything forever. Storage is free.

Can my HSA provider help if I get audited?

They can give you dates, amounts, and vendor names. But they cannot tell the IRS what you bought. That is your job.

This is educational content, not financial or tax advice. Consult a qualified professional before making decisions about your HSA.